深層地熱:潔淨能源的技術演進與政策挑戰

技術探索

2025-07-25

作者:Marc Anthonisen, MPA/永續科學中心淨零科技工作小組

(中文僅為英文全文摘要。)

深層地熱(deep geothermal)是一種具潛力的次世代潔淨能源技術,特別適用於如臺灣這類位於火環地帶的地熱區域(“Ring of Fire”)。與傳統淺層地熱不同,深層技術需透過超過一公里的深井擷取熱能,用以回應減碳與電力需求的雙重壓力。

目前已有印尼、肯亞、菲律賓等國發展深層地熱,美加企業也陸續簽署購電協議(power-purchase agreements, 2024),進入早期商業化階段。此進展受惠於政府對鑽井研發的投資,以及油氣產業累積的鑽探能力。

美國能源部指出,若深層地熱全面開發,可供應達90GW電力,為未來能源結構的一部分。

成功發展深層地熱需突破技術與營運瓶頸,關鍵包括:提升鑽井效率、導入先進感測系統(remote sensors, fiber optics, AI mapping)、控制誘發地震風險(induced seismicity),以及建立材料、人力、設備供應鏈等完整生態系。

目前主流開發路徑包括:

增強型地熱(Enhanced Geothermal):採用水力壓裂創造裂縫,提升井間熱交換效率。

先進型地熱(Advanced Geothermal):建立封閉循環管線,提高水流控制性。

超高溫地熱(Superhot Rock / Supercritical Geothermal):鑽探超過7公里、取用高於375°C的熱源(>7km, >375°C, supercritical phase)。

技術商轉仍面臨高額前期成本與不確定性,需透過政策協助進行「去風險化」(derisking),以吸引私人資本投入並穩定成本結構。另方面,法規、環境許可與社區溝通也將影響此技術推動的公平性與可行性。

Deep Geothermal Energy: Technology and Policy for Clean Power

Author: Marc Anthonisen, MPA/Net Zero Technology

(Full English text)

Geothermal energy, particularly “deep” geothermal, at well depths over a kilometer, is a promising technology for producing clean energy (WRI, 2024). As a volcanic island on Asia-Pacific’s “Ring of Fire,” Taiwan possesses geologic reserves of heat energy that can potentially be tapped to generate electricity in the future. However, deep geothermal is still in its early stages and requires significant development of technology and drilling techniques before it can be deployed at scale. Moving up this technological learning curve will be the key to deploying this technology to mitigate climate impacts.

Geothermal energy has already been used to generate electricity for many decades, but only at shallow depths where the earth’s heat is readily accessible. This is what is called “traditional” or “conventional” geothermal (National Academies, 2024). Newer approaches aim to go much deeper to access heat energy instead of waiting for it to rise to the surface. Many countries are already developing deep geothermal, including Indonesia, Kenya, and Philippines (IEA, 2024). Some companies from the US and Canada have also recently also made progress in developing geothermal for power generation, with several new power-purchase agreements being finalized in 2024 (Galluci, 2024). This early success is in part due to government investments in drilling research, and in part due to recent advances in drilling capabilities in the North American oil and gas sector (WRI, 2024).

Tech giants Google and Meta have both recently signed deals to acquire electricity from geothermal startups in the US. At the same time, a California electric utility has contracted to acquire electricity from a new geothermal plant in Nevada (Galluci, 2024). These are in fact just initial deals as the industry starts to shift from research into commercialization before reaching its full-scale potential. The US Department of Energy estimates that if geothermal is fully developed, it could supply over 90GW of energy out of the 700-900GW that could be needed in the US by 2050 (US DOE, 2024).

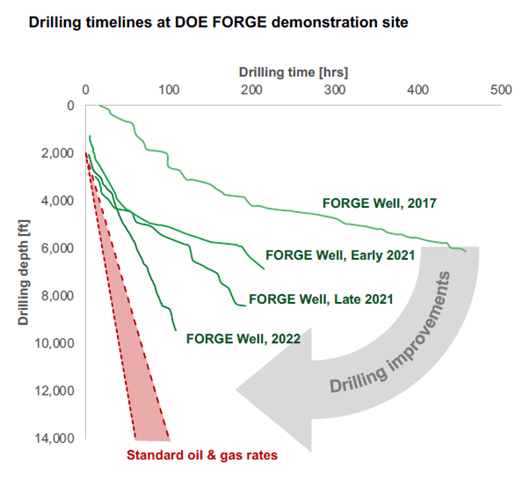

Learning curve

Locating reservoirs of heat many kilometers below the surface of the earth often requires drilling multiple wells. Thus, how quickly a well can be drilled is a critical success factor for developing geothermal. At a test facility in Utah called FORGE, the US Department of Energy has continually improved on drilling times. These advances are being shared with nearby private sector startups such as Fervo Energy, which now has two commercial geothermal power operations in both Utah and Nevada (US DOE, 2024).

Enhanced Geothermal Liftoff Report (US DOE, 2024)

Another key factor includes developing remote sensors that can help map the geological formations. Increasingly this involves using technologies like fiber optics as well as artificial intelligence to create an accurate picture of geothermal assets (Venketeswaran et al, 2022). Sensor technology is also essential in minimizing “induced seismicity,” in other words the risk of generating earthquakes (Hudson et al., 2024).A final critical success factor for deep geothermal is the development of an entire ecosystem of capabilities, including equipment suppliers, specialty materials, and trained personnel. This ecosystem also takes time to develop. A period of continuous testing is essential to building up these capabilities (US DOE, 2024).

- Different ways to access underground heat

The model being used by Fervo is what is known as “Enhanced Geothermal.” It uses hydraulic fracturing, or “fracking,” to create fissures and provide a horizontal pathway for water to move between one well and another. This maximizes the surface area of hot rocks that can be accessed. This approach has been used to access natural gas in US but can now be used to tap geothermal (US DOE, 2024).

Another approach is creating a closed loop of pipes in what is called “Advanced Geothermal.” Canadian startup Eavor is using this approach in Germany to supply electricity. The benefit of this approach is improved control of liquids flowing between wells. Long horizontal “forks” of pipes are being drilled in parallel to again maximize the exposure to heat reservoirs (National Academies, 2024).

A third approach is what is called “Superhot Rock” or “Supercritical” Geothermal (Seligman, 2025). This involves drilling over 7km down to where geothermal resources are widely available at temperatures above 375C. At this temperature, water reaches a new “supercritical” phase that packs much more energy than liquid water or steam. However, the deeper well will increase the up-front capital costs. As a result, this technology is still in the test stage (Hao, 2025; “Mazama Energy”, 2024), even though advocates promote its eventual lower running costs and broader accessibility (Seligman, 2025).

Financing

In addition to the technical and logistical challenges of developing deep geothermal is a financial one. As a relatively new, capital-intensive technology, geothermal requires significant amounts of up-front capital to develop the new technologies and finance the drilling of new wells. Once these stages are overcome, the technology will become more stable and average costs will come down as more and more power demand comes online. Encouraging private sector capital to invest in this early stage is one of the major challenges for any new technology and an area where governments can try to reduce barriers. This stage is thus often referred to as “derisking.” The goal is to help the technology develop to the point where investors and commercial banks are comfortable providing continuous operating capital (US Department of Energy, 2024).Regulations, Permitting, and Equity

Deep geothermal is a new technology. As such environmental and land-use regulations may need to be updated to clear a path for implementation. Changes to permitting rules may be yet another key step in bringing this technology online (Cariaga, 2025; Streater, 2024). At the same time, the approach needs to respect the land and communities of the people involved. Any new technology comes with new environmental impacts as well as impacts on surrounding communities. Partnering with local communities to ensure an equitable and engaged approach is yet another key to successful geothermal implementation (Abdi et al. 2024).

References

- Abdi, A. M., Murayama, T., Nishikizawa, S., Suwanteep, K., & Obuya Mariita, N. (2024). Determinants of community acceptance of geothermal energy projects: A case study on a geothermal energy project in Kenya. Renewable Energy Focus, 50, 100594. https://doi.org/10.1016/j.ref.2024.100594

- Cariaga, C. (2025, February 12). Mexican President proposes revamped geothermal law as part of energy reforms. Think Geoenergy. https://www.thinkgeoenergy.com/mexican-president-proposes-revamped-geothermal-law-as-part-of-energy-reforms/

- Galluci, M. (2024, December 20). Was 2024 a breakout year for next-generation geothermal energy? Canary Media. https://www.canarymedia.com/articles/geothermal/was-2024-a-breakout-year-for-next-generation-geothermal-energy

- Hao, C. (2025, January 30). Houston startup Quaise Energy aims to drill deeper than ever before to harness geothermal energy. Houston Chronicle. https://www.houstonchronicle.com/business/energy/article/quaise-energy-demonstrates-drilling-technology-20061849.php

- Hudson, T. S., Kettlety, T., Kendall, J.-M., O’Toole, T., Jupe, A., Shail, R. K., & Grand, A. (2024). Seismic Node Arrays for Enhanced Understanding and Monitoring of Geothermal Systems. The Seismic Record, 4(3), 161–171. https://doi.org/10.1785/0320240019

- International Energy Agency. (2024). The Future of Geothermal Energy. https://iea.blob.core.windows.net/assets/fe8d11b6-b1a6-43d9-9351-47d86ed1dfbc/TheFutureofGeothermal.pdf

- Mazama Energy receives $20 million Dept. Of Energy grant to test super-hot rock geothermal system at Newberry Volcano. (2024, December 20). KTVZ21. https://ktvz.com/news/business/2024/12/20/mazama-energy-receives-20-million-dept-of-energy-grant-to-test-super-hot-rock-geothermal-system-at-newberry-volcano/

- National Academies - Earth and Life Studies. (2024, November 20). Advancing Geothermal Energy [Youtube]. https://www.youtube.com/watch?v=C20N_wSRDSM

- Seligman, A. (2025). An introduction to the next clean energy frontier: Superhot rock geothermal and a vision for firm, global clean energy. Clean Air Task Force. https://www.catf.us/2025/01/introduction-next-clean-energy-frontier-superhot-rock-geothermal/

- Streater, S. (2024, October 17). BLM approves massive geothermal project, moves to ease permitting. E&E News. https://www.eenews.net/articles/blm-approves-massive-geothermal-project-moves-to-ease-permitting/

- US Department of Energy (DOE). (2024). Pathways to Commercial Liftoff: Next-Generation Geothermal Power. https://www.nrel.gov/geothermal/next-generation

- Venketeswaran, A., Lalam, N., Wuenschell, J., Ohodnicki, P. R., Badar, M., Chen, K. P., Lu, P., Duan, Y., Chorpening, B., & Buric, M. (2022). Recent Advances in Machine Learning for Fiber Optic Sensor Applications. Advanced Intelligent Systems, 4(1), 2100067. https://doi.org/10.1002/aisy.202100067

- World Resources Institute (WRI). (2024). Next-Generation Geothermal: Considerations and Opportunities for Responsible Development. https://doi.org/10.46830/wriib.24.00015